On November 13, 2025, the IRS released the cost-of-living adjustments to retirement plan contribution limits for the 2026 tax year.

These annual updates are required under the Internal Revenue Code and reflect changes in inflation and other economic factors.

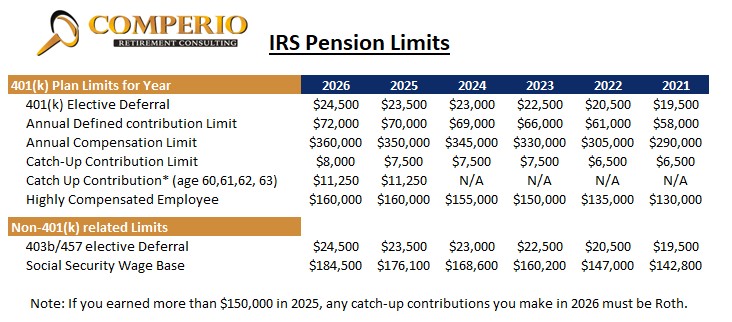

Some highlights are:

- Employee 401(k) deferral limit increases to $24,500 (from $23,500).

- Age-50+ catch-up contribution limit increases to $8,000, and the special age 60–63 catch-up remains $11,250.

- Total 401(k) contribution limit (employee + employer) increases to $72,000.

- Compensation cap for 401(k) purposes increases to $360,000, while the Highly Compensated Employee (HCE) threshold stays at $160,000.

- Mandatory Roth catch-up for higher earners, with a higher wage threshold:

- Beginning in 2026, participants age 50+ whose 2025 FICA wages from the plan sponsor exceed the Roth catch-up wage threshold must make all 2026 catch-up contributions as Roth (after-tax) contributions.

- The IRS has now increased that wage threshold for 2025 pay from $145,000 to $150,000. This means any participant who earns more than $150,000 from the employer in 2025 can only make Roth catch-up contributions in 2026.

* Due to new Secure 2.0 optional provision

Comperio Retirement Consulting has been named one of the largest 100 Investment Consultants in the United States according to Pension & Investments (P&I) for the past 8 years

Comperio Retirement Consulting has been named one of the largest 100 Investment Consultants in the United States according to Pension & Investments (P&I) for the past 8 years