We ended March with considerable resilience in U.S. financial markets. While returns remain below earlier highs and policy signals are somewhat uncertain, markets have remained relatively stable.

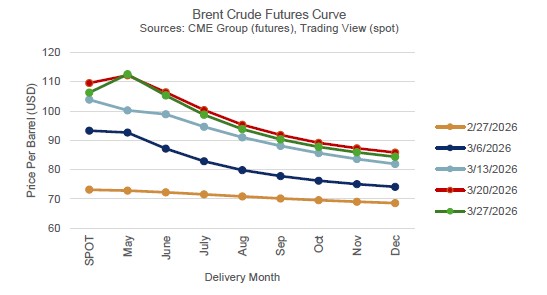

Brent crude prices have risen sharply, moving from the low-$70s in late February to roughly $100+ by month-end. The entire futures curve has shifted higher alongside spot but remains clearly downward sloping (“backwardated”), with prices declining into the low-$80s by year-end. Also note that aside from the first week of the war (ending 3/6), the longer-term expectations have remained consistent since the outset.

That shape is important. Markets are signaling tight near-term supply conditions, but not a lasting shortage. In practical terms, while current energy prices reflect real short-term pressure, futures pricing suggests those pressures are expected to ease over time—implying limited additional upside to inflation from oil beyond current levels.

Comperio Retirement Consulting has been named one of the largest 100 Investment Consultants in the United States according to Pension & Investments (P&I) for the past 8 years

Comperio Retirement Consulting has been named one of the largest 100 Investment Consultants in the United States according to Pension & Investments (P&I) for the past 8 years