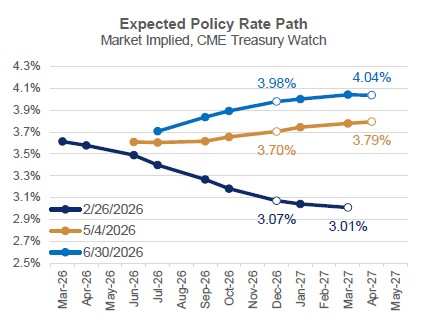

Kevin Warsh, the new Fed Chair, explicitly stated the Fed would no longer provide ‘forward guidance’. Nevertheless, pundits reported that Warsh signaled future rate hikes. Similarly, but not necessarily an endorsement of pundits, markets have priced in a single ¼ point rate increase by year-end. Expectations for the policy rate at year-end are now nearly a full percentage point higher than they were four months ago, despite fading tariff impacts and retreating oil prices. Compare:

As of 2/26/2026 – days prior to the war in Iran, tariff uncertainty was the primary focus on the inflation front, and the one-time step-up in prices had nearly run its course. Brent crude oil futures prices were trading in the upper $60s per barrel. Year-end expectations for Fed Funds was just above 3%.

As of 5/4/2026 – the highest closing price for Brent Crude futures, at just below $115/barrel; oil price shocks have become the largest inflation concern for policymakers. The expected policy rate at year end was near 3.75%.

As of 6/30/2026 – reports of an agreement between the US and Tehran and a fully reopened Strait caused oil prices to retreat to the low $70’s/barrel. Yet market expectations for policy rates rose to nearly 4%, above expectations when oil prices were trading 50% higher.

Comperio Retirement Consulting has been named one of the largest 100 Investment Consultants in the United States according to Pension & Investments (P&I) for the past 8 years

Comperio Retirement Consulting has been named one of the largest 100 Investment Consultants in the United States according to Pension & Investments (P&I) for the past 8 years